Once the Model 720 declaration has been submitted regarding one or more of the reporting obligations contained therein (the three categories: real estate, bank accounts, and other assets), it will only be necessary to resubmit this model when, in relation to one or more of these obligations, there is an increase in the overall threshold established for each block of information exceeding €20,000 compared to the amount that determined the submission of the last declaration.

Example based on a consultation to the tax administration:

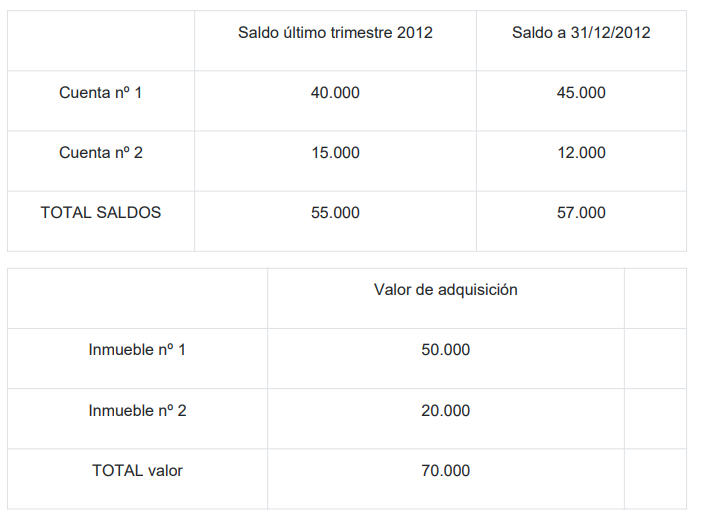

Model 720 was submitted in fiscal year 2013, based on information from fiscal year 2012. This informative declaration reported bank accounts in financial institutions located abroad and real estate abroad, with the following balances and values:

There will again be an obligation to submit the informative declaration, Model 720, in subsequent fiscal years when there is an increase in the overall threshold established for each block of information exceeding €20,000 compared to the amount that determined the submission of the last declaration.

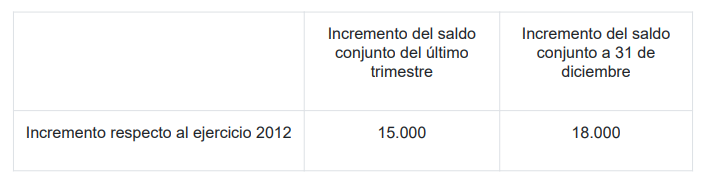

Fiscal Year 2013: If in fiscal year 2013, the values of the real estate do not change substantially, even considering variations due to exchange rates (and no other cause arises that would require its declaration, such as its sale), the combined balance of all accounts in the last quarter increases by €15,000, and the combined balance of all accounts as of December 31 increases by €18,000, resulting in the following total balances:

The increases in the combined balances of the accounts have been as follows:

In fiscal year 2013, there will be no obligation to submit Model 720 regarding the obligation to report on real estate located abroad (Article 54 bis of the General Regulations approved by RD 1065/2007, dated July 27). Likewise, there is no obligation to submit Model 720 regarding the obligation to report on accounts in financial institutions located abroad (Article 42 bis of the General Regulations approved by RD 1065/2007, dated July 27) since neither the combined balance (total) in the last quarter nor the combined balance (total) as of December 31 increased by more than €20,000 compared to the amounts that determined the obligation to declare in the last fiscal year of its submission, in this case, the previous year (provided that no other cause exists that would require its submission, such as the sale or cancellation of any of them).

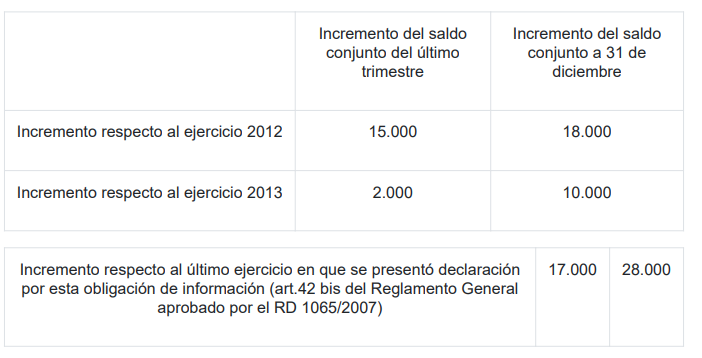

Fiscal Year 2014: If in fiscal year 2014, the combined balance of all accounts in the last quarter increases by €2,000 and the combined balance of all accounts as of December 31 increases by €10,000. The increases in balances for each year and overall are as follows:

The increase that must be taken into account is the increase in the combined balance of the last quarter and the combined balance as of December 31 compared to the balances that determined the obligation to report on accounts in financial institutions located abroad (Article 42 bis of the General Regulations approved by RD 1065/2007, dated July 27) in the last fiscal year in which it was submitted.

In this case, the increase in the combined balance as of December 31, 2014, compared to the combined balance as of December 31 of the last fiscal year in which the Model 720 declaration was submitted for this reporting obligation, has exceeded €20,000. Therefore, for fiscal year 2014, an informative declaration, Model 720, must be submitted regarding the obligation to report on all accounts in financial institutions located abroad.